By Jan Nieuwenhuijs of Gainesville Coins

This article is a primer on the Chinese gold market, more specifically the Shanghai International Gold Exchange (SGEI). The SGEI facilitates “offshore” gold trading in renminbi and can play a crucial role in de-dollarization, as it allows countries to use renminbi as a trade currency that can be converted into gold without affecting China’s balance of payments. De-dollarization can be accomplished by using yuan to settle international trade and store surpluses in gold through the SGEI.

Introduction

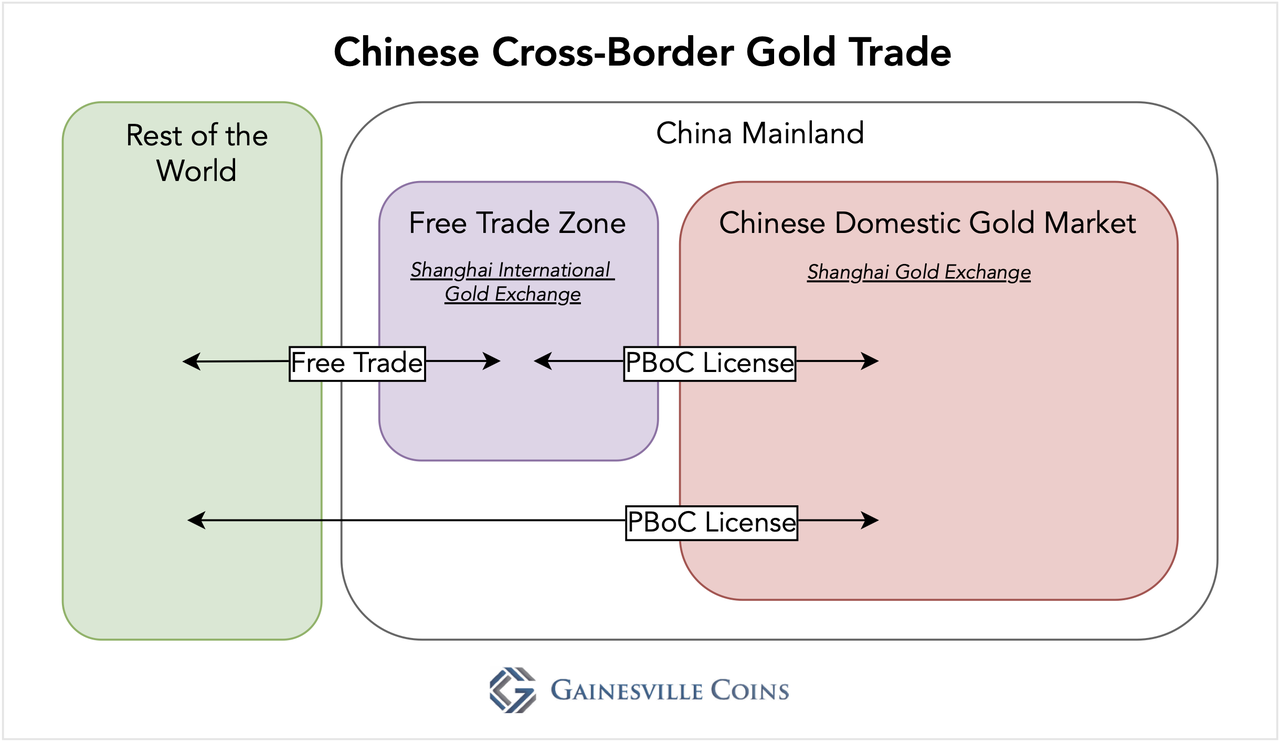

In the Chinese gold market two circuits can be distinguished. Simplified, there is gold trading in the domestic market and in Free Trade Zones (FTZs). The domestic market is separated from FTZs and the rest of the world by the Chinese central bank, the People’s Bank of China (PBoC), that controls import into and export from the domestic market. Gold import and export between FTZs and the rest of the world is not regulated by the PBoC. The SGEI is located in the Shanghai Free Trade Zone (SFTZ) to spur international gold trading in renminbi.

The Chinese Domestic Gold Market

Let’s first examine the Chinese domestic gold market with the Shanghai Gold Exchange (SGE) at its core before we discuss the ins and outs of the SGEI.

Prior to 2002 the PBoC was the primary dealer in the Chinese gold market. With the launch of the Shanghai Gold Exchange (SGE) in 2002 the market was slowly liberalized and took over price setting and gold allocation from the central bank. By 2007 liberalization was completed as by then most wholesale supply and demand flowed through the SGE.

Laws and tax incentives funnel most supply—mine output, imports, and recycled gold—towards the SGE, which for liquidity reasons automatically attracts most demand. The SGE has its own chain of integrity, meaning only certified refineries can load-in gold bars into SGE vaults. To guarantee all metal in the SGE vaulting system is of the right quality, bars withdrawn from the vaults are not allowed to re-enter before having been remelted by a certified refiner. Every month the SGE publishes the tonnage of gold withdrawn from its vaults, which can be interpreted as wholesale demand.

From the SGE rulebook:

gold bullion will no longer be accepted into any [SGE] Certified Vault once it has been withdrawn by a member or customer.

Import into and export from the domestic market is referred to as “general trade,” and in the case of gold it’s controlled by the PBoC. Twenty or so enterprises are authorized to import and export standard gold*, but for every batch they need a new License by the PBoC. Because the Chinese government has a policy of storing gold among the people to strengthen China’s economic security, imports are usually not restricted, as opposed to exports that are more or less prohibited. Panda Coins, for example, will be allowed to be exported from the domestic market, but that’s about it.

Since 2004 jewelry fabricators and alike located in mainland China can sell their products abroad though “processing trade.” For processing trade no PBoC License is required; under this framework enterprises can freely import into and export gold from FTZs. A fabricator can import raw materials into a FTZ, manufacture products, and export the finished goods. Needless to say, any entity wanting to import gold from a FTZ into the domestic market needs approval by the PBoC.

The Shanghai International Gold Exchange

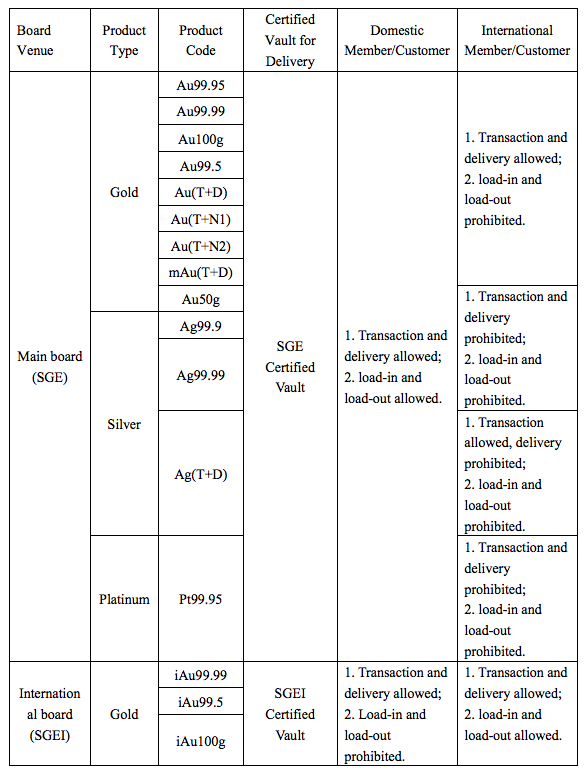

To slowly open up China’s financial markets, enhance the connection between the international gold market and the Chinese domestic market, and push renminbi internationalization the SGEI was launched in 2014 in the SFTZ. The SGE is often referred to as the Main Board (MB) and the SGEI as the International Board (IB). The SGEI is fully owned by the SGE (the Exchange hereafter).

Both foreign and Chinese residents can trade MB as well as IB gold contracts on the Exchange. Though, foreigners can only load-in and load-out gold into and from IB vaults in the SFTZ, while Chinese residents can only load-in and load-out gold into and from MB vaults in the domestic market. The exception is that those eligible to import gold under general trade may sell gold located in IB vaults into the domestic market**. Below is an overview of what privileges which traders have with respect to MB and IB contracts.

Foreigners and Chinese residents can thus add liquidity to MB and IB contracts but can only physically move metal on their own side of the fence. As a result, neither will trade gold on the other side for reasons other than making markets, arbitrage, and speculation. Chinese long-term investors, in example, are not likely to buy metal in the SFTZ as they can’t withdraw that metal. Foreigners wanting to withdraw and repatriate will trade IB contracts.

Another feature of the Exchange is that it commingles onshore and offshore renminbi, providing a platform for arbitrage between the two.

China’s Balance of Payments, Cross-border Trade Statistics, and SGE Withdrawals

To understand everything related to the SGEI, we need to drill a little deeper into international trade. What is often misunderstood is that a country’s current account—part of its Balance of Payments, BOP—is not a reflection of goods and services crossing its border. Current accounts register the value of goods and services exchanged between domestic and foreign residents, wherever these residents are located. Cross-border trade statistics (International Merchandise Trade Statistics, IMTS), on the other hand, record the value of goods physically being moved across borders irrespective of the buyer and seller’s nationalities.

Should a European bullion bank ship gold from London to an SGEI vault in the SFTZ, this will show up in global IMTS but doesn’t affect China’s BOP. When this batch is bought by an Indian investor, withdrawn from an SGEI vault, and exported to a designation of the owners’ discretion, the trade has circumvented China’s current account although it was settled with yuan. To be clear, for IMTS data it’s irrelevant if goods are shipped into a FTZ or the domestic market, as long as it crosses an international border an import and export are recognized.

Now we have reached a basic understanding of the SGEI, we need to examine a few additional elements to complete our analysis. Regarding IMTS figures, only non-monetary gold movements across borders are recorded. Monetary gold, which is metal owned by a monetary authority such as a central bank, is exempt from being reported in IMTS. From the United Nations IMTS rulebook:

Since monetary gold is treated as a financial asset rather than a good, transactions pertaining to it should be excluded from international merchandise trade statistics.

We could be misled when reviewing Chinese net import, in example, if a bank imports gold into the SFTZ, which is then bought by the central bank of Saudi Arabia (SAMA) on the SGEI, and then invisibly exported as monetary gold. The moment SAMA buys non-monetary gold, the metal is monetized—as prescribed by the IMF—and is subsequently eclipsed from cross-border trade statistics. This is how central banks move gold across the globe under the radar. IMTS would display the non-monetary gold import into China but not the monetary gold export, leading to an overstatement of Chinese net import. The reverse is also true: a central bank shipping monetary gold to the SFTZ would be invisible until it is bought by the private sector and de-monetized.

In final, the Exchange discloses an aggregate number for the monthly weight of gold withdrawn from SGE and SGEI vaults combined. At the surface, this number is difficult to put into perspective. Total load-out volume could all end up in the domestic market—being a useful reflection of Chinese wholesale demand—or a chunk of it is exported as (non-)monetary gold from the SFTZ. Luckily, I have insider knowledge from a source at the SGEI. In 2015, this person told me that virtually all IB trading was done by Chinese banks for importing gold into the domestic market. More recently he wrote me that little gold withdrawn from IB vaults is exported abroad. Total withdrawals thus mainly relate to Chinese demand.

Conclusion

As demonstrated, gold trading in renminbi on the SGEI can be compared to offshore gold trading in the London Bullion Market with US dollars. As such, the SGEI is part of China’s ambitions to internationalize the renminbi to the detriment of the dollar.

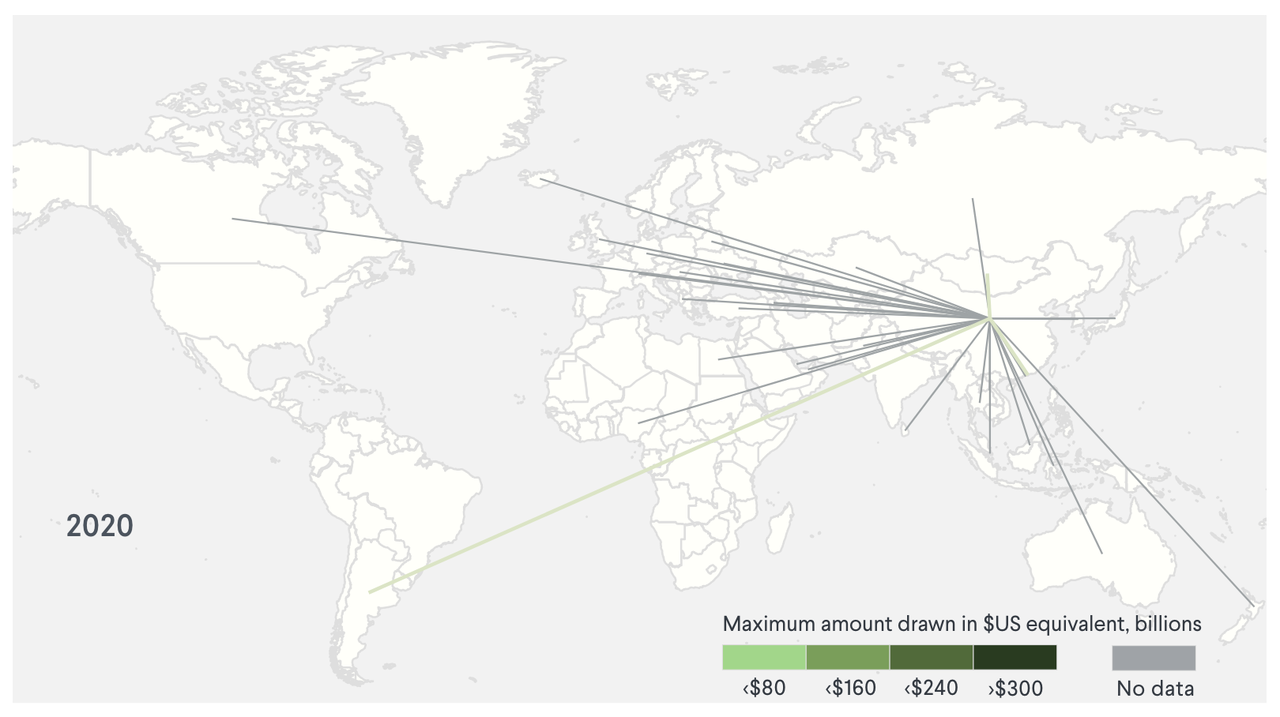

Many commentators in the financial blogosphere state China’s closed capital account is holding back the offshore renminbi market from competing with the Eurodollar (offshore dollar) market. True, though PBoC swap lines promote the international use of renminbi, and as Zoltan Pozsar noted in the In Gold We Trust 2023 report: “China has a swap line with everybody.” With which he meant thirty-two counterparties.

Confirming what we have discussed is a speech by Teng Wei, Deputy General Manager of the Shanghai International Gold Exchange, from 2016:

The international board uses renminbi for pricing and settlement, which effectively connects the onshore and offshore renminbi market …. It also provides a new channel for the return of funds, which is a useful exploration for expanding the cross-border flow of renminbi and steadily promoting the internationalization of renminbi.

…

The journey of the Shanghai International Gold Exchange will epitomize the opening of China’s financial markets to the outside world and play an important part in the internationalization of the renminbi. With Shanghai becoming the third most important market in the world after London and New York, the Chinese gold market will make a great contribution to the internationalization of the renminbi.

Renminbi reserve currency status is still far away because yuan held overseas can’t freely be invested in Chinese assets such as bonds and other securities due to China’s closed capital account. Renminbi can, however, be converted into gold without limits.

Last month Russian news outlet TASS reported the BRICS nations are working on a common currency for international payments. “The idea of creating a common currency, although I would probably call it a payment unit inside BRICS countries, is floating around and is being discussed. We also have proposals about using digital financial assets supported by real assets, for example gold stable coins,” Russia’s Finance Minister Anton Siluanov said.

These gold stable coins are most likely to represent gold held in SGEI vaults, Moscow, or other cities in Brazil, South-Africa, or India. Time will tell if the BRICS will materialize this new payment system that incorporates gold, and if the SGEI will be used more by international players.

Appendix

* In China standard gold must be a bar or ingot weighing 50g, 100g, 1Kg, 3Kg or 12.5Kg, with a minimum fineness of 995.0, 999.0, 999.5, or 999.9 parts per thousand.

** Technically, an enterprise eligible for import may load-in metal into IB vaults and sell these metals as deliverable on the MB, provided it has a PBoC License. When the buyer wants to withdraw this gold, the Exchange will make sure it will be loaded out from a vault in the domestic market. That is the easy way of explaining it. For the exact rules please read the Detailed Delivery Rules of Shanghai Gold Exchange:

The Exchange has established a network of Certified Vaults to facilitate physical delivery through the Exchange as well as bullion storage and other transactions by members and customers. Certified Vaults are classified into Main Board Certified Vaults (the MB Certified Vaults) and International Board Certified Vaults (the IB Certified Vaults). MB Certified Vaults provide bullion storage, load-in and load-out services to Domestic Members and Domestic Customers. IB Certified Vaults provide bullion storage, load-in and load-out services to International Members, International Customers, and any Domestic Members and Domestic Customers who are qualified to import and export gold [have a PBoC License], as well as in acting as their agent in making customs declarations for bullion to be transported into or out of bonded zones [FTZs]. IB Certified Vaults shall accept the supervision of the customs authorities of China.